With the government announcing major home loan reforms and property prices growing strongly in many parts of the country, there’s a lot happening right now:

- Govt unveils mortgage reforms

- How many loans have under 20% deposit?

- City-by-city property prices

- SMSF tax return guidance

Govt Wants Consumers to “Get a Better Deal” on Their Mortgage

The federal government has unveiled a series of reforms to the banking sector, which aim to help consumers access lower home loan rates and higher savings accounts rates.

As part of the reforms, Treasury will investigate how behavioural economics could be used in the banking sector to encourage consumers to switch to cheaper home loans and banking products.

Also, lenders will be required to make it easier for customers to refinance their mortgage, by ensuring they have direct and easy access to the forms needed to switch.

Treasurer Jim Chalmers said these changes would “help bank customers get a better deal, including through more choice, lower prices and better services”. For consumers, that could mean:

- Getting alerted about lower-rate home loan options

- Being nudged to think about refinancing to a better home loan

- Having an easier, faster refinancing process

Those outcomes, if they occur, would be welcome, because the essence of a broker’s role is to make it easy for consumers to compare loans and, when necessary, refinance to a more suitable loan.

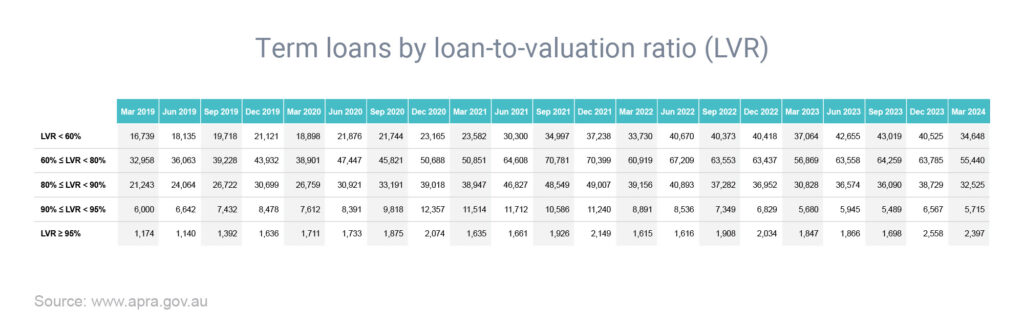

31% of Borrowers Have Less Than 20% Deposit

While it’s often said you need a 20% deposit to qualify for a home loan, a significant number of borrowers are securing mortgages with smaller deposits, according to the latest data from APRA, the banking regulator.

In the March 2024 quarter, 31.0% of new home loans (by value) had deposits of less than 20%, while 6.2% of new loans had deposits of less than 10%.

Generally, you will need to pay lender’s mortgage insurance (LMI) if you purchase a property with a deposit of less than 15-20%. However, some lenders give LMI exemptions to certain professionals, such as doctors, dentists, physiotherapists, lawyers and accountants.

While more than three in 10 borrowers are taking out loans with deposits under 20%, these figures are relatively low by historical standards. Back in December 2020, for example, 41.7% of new loans had deposits of less than 20%, while 11.3% had deposits of less than 10%.

This illustrates how banks have tightened their lending standards, to ensure borrowers don’t take on an excessive amount of debt.

Yet it’s still possible to buy a property with a small deposit, provided your financial circumstances allow it and you structure your loan application correctly.

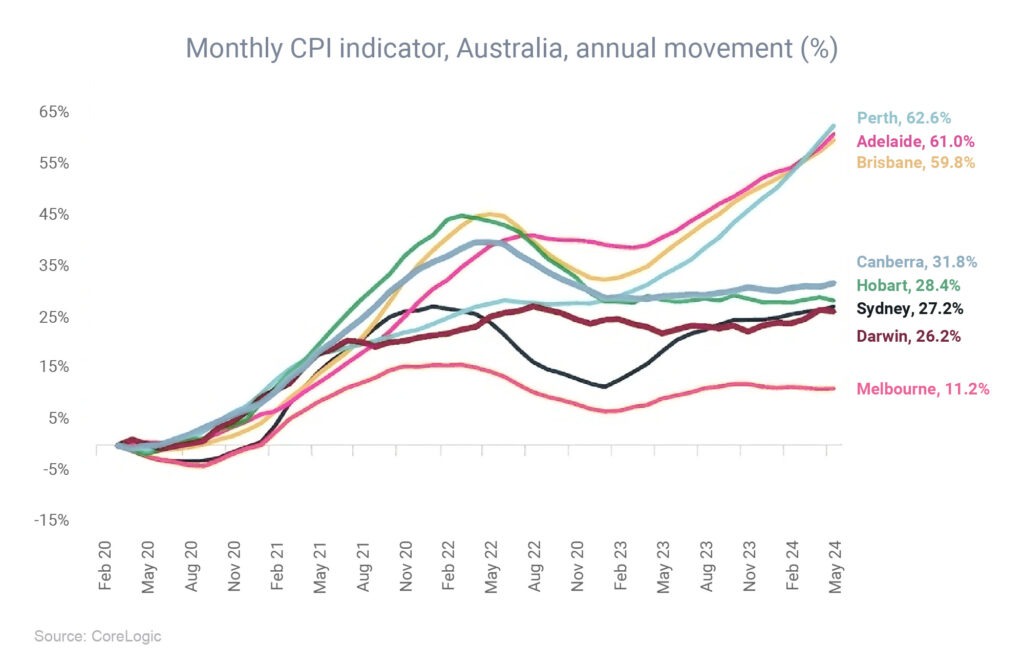

Why Property Price Growth Is So Varied Throughout Australia

The Australian property market is growing briskly right now and has grown significantly since the pandemic. But the city-by-city performance has been more varied.

Over the year to May, the national median price rose 8.3%, according to CoreLogic. But at a city level, growth ranged from a staggering 22.0% increase in Perth to a 0.1% decrease in Hobart.

Meanwhile, growth since March 2020 has ranged from a high of 62.6% in Perth to a low of 11.2% in Melbourne.

CoreLogic’s head of research, Eliza Owen, attributed the contrasting results to diverse market conditions.

“The highest-performing markets have generally come off a low base, with housing conditions and demographic trends relatively weak over the years preceding the pandemic,” she said.

“Differences in capital growth trends are marked by the varied supply-demand balances of each city, and in turn migration, affordability factors and dwelling completions influence that supply and demand dynamic.”

Ms Owen said annual growth had started to slow across the combined capital cities. “This could mean a slowdown in growth across Brisbane, Perth and Adelaide is on the horizon, and could see the range of growth eventually narrow across the capital cities,” she added.

How to Get Your SMSF Tax Return Right

If you’re one of the many Australians who’ve purchased a property through a self-managed superannuation fund (SMSF), the Australian Taxation Office (ATO) has provided valuable guidance about how to file your annual tax return.

The ATO said that if you want your SMSF annual return to be processed without delay, you should make sure:

- You include members’ information and tax file numbers (in Section F).

- You provide the correct SMSF auditor number and auditor details, including the date the audit was completed (Section A Item 6).

- The closing account balance equals the sum of accumulation and retirement phase account balance amounts. If the member’s closing account balance is zero or a negative amount, write 0 (Section F Label S).

If you want to wind up your SMSF and lodge your final return, you should make sure you have paid member benefits if a condition of release has been met or rolled over funds to an APRA account via SuperStream, according to the ATO.