Land tax is a recurring charge levied by the state government on the ownership of land. The main goal of this tax is to raise funds for public amenities and infrastructure projects, guaranteeing that landowners support the state’s development and maintenance.

At Unconditional Finance, we prioritise providing our clients with the latest updates and comprehensive advice on financial and property tax matters. Our team of experienced mortgage brokers in Sydney are here to guide you through these changes, ensuring that your financial strategies remain effective and aligned with the new regulations.

In Victoria, land tax applies to all properties above a specific value threshold, with the tax rate escalating based on the total taxable value of the land owned. This system is designed to make sure landowners pay a fair amount of tax based on the value of their land.

Earlier this year, the State Revenue Office of Victoria commenced issuing land tax assessment notices for the 2024 land tax year.

This year, many taxpayers are experiencing substantial increases in their land tax liability because of higher land tax rates and the increased valuations being ascribed to properties.

New Land Tax Rates and Thresholds

Starting in 2024, the Victorian Government will implement revised land tax rates and thresholds. These changes reflect the state’s evolving economic landscape and aim to ensure that the tax system remains equitable and responsive to market conditions. The new rates will be higher for premium properties, thereby increasing the tax obligations for owners of high-value lands.

The revised rates and thresholds will result in varied impacts across different property owners. Owners of high-value properties will experience an increase in their land tax liabilities, while some middle-tier properties might see minimal changes. This adjustment seeks to balance revenue generation with fair tax distribution among landowners.

Commercial and Industrial Property Tax (CIPT)

The Commercial and Industrial Property Tax (CIPT) will be introduced on 1 July 2024, replacing the current stamp duty for commercial and industrial properties. CIPT will be an annual tax based on the value of the property, shifting from a one-time transaction cost to a recurring tax burden. This move aims to stabilise government revenue and promote long-term investment planning.

The shift from stamp duty to CIPT represents a significant change in how commercial and industrial properties are taxed. This transition is designed to reduce the upfront costs associated with property transactions, encouraging more frequent buying and selling activities. Business owners will need to adjust their financial strategies to account for the ongoing CIPT payments.

Vacant Residential Land Tax (VRLT) Modifications

Expanded Exemptions for Holiday Homes and Properties Owned by Companies and Trusts

Modifications to the VRLT will include expanded exemptions, particularly benefiting owners of holiday homes and properties held by companies and trusts. These changes acknowledge the diverse usage of residential properties and aim to alleviate the tax burden on non-primary residences that serve other functional purposes.

New Criteria and Implications for VRLT

The new VRLT criteria will simplify the compliance process for property owners, ensuring that only genuinely vacant properties are taxed. This adjustment seeks to make the tax system more fair and efficient, reducing unnecessary financial strain on owners of occasionally vacant properties.

Apportionment of Land Tax and Windfall Gains Tax

The apportionment rules for land tax and windfall gains tax will be revised to ensure a more precise calculation of tax liabilities. These changes will impact properties undergoing development or significant value increases, aiming to reflect their current market value more accurately.

These new rules will significantly affect high-value property transactions and developments. Property owners and developers will need to consider these apportionment changes in their financial planning to mitigate potential tax liabilities during property sales or developments.

COVID Debt Repayment Plan Adjustments

The COVID Debt Repayment Plan was introduced to assist property owners in managing their tax liabilities during the economic downturn caused by the pandemic. This plan allowed for deferred tax payments and provided financial relief to those severely impacted by COVID-19.

Adjustments to the COVID Debt Repayment Plan will include revised repayment schedules and potential tax reductions for eligible property owners. These changes are designed to ease the financial burden and support the recovery of affected businesses and individuals.

Abolition of Land Transfer Duty on Commercial and Industrial Properties

The abolition of land transfer duty for commercial and industrial properties, effective from 1 July 2024, is a significant policy shift. This change aims to eliminate the upfront tax costs associated with property transactions, replacing it with the ongoing CIPT.

The expected benefits include lower initial costs for businesses acquiring property, fostering economic activity and investment in the commercial and industrial sectors. The transition process will involve a phase-out of stamp duty and the implementation of CIPT, requiring businesses to adapt to the new tax regime.

Other Property-related Tax Changes

Adjustments to Various Land and Property Taxes

Several related taxes, such as the Growth Areas Infrastructure Contribution (GAIC) and the Metropolitan Planning Levy (MPL), will undergo adjustments in alignment with broader tax reforms. These changes aim to streamline tax obligations and ensure consistency across the property tax system.

The specific changes will include rate adjustments and revised criteria for these taxes, potentially reducing the financial burden on developers and property owners. These reforms are intended to support sustainable development and equitable tax distribution.

Prohibitions and Exemptions

New regulations will prohibit property sellers from transferring land tax and windfall gains tax obligations to purchasers. This measure ensures transparency and fairness in property transactions, protecting buyers from unexpected tax liabilities.

Updated exemption criteria will provide clearer guidelines for property owners, helping them understand their tax liabilities and potential relief options. These changes aim to simplify the tax compliance process and ensure that exemptions are applied fairly.

Calculating Your Land Tax

To calculate your land tax with the new changes, it’s best to use the Victorian Government’s Land Tax Calculator, as it includes the updated rates and thresholds. This tool can help you get a more precise estimate by taking into account your specific property values and ownership details.

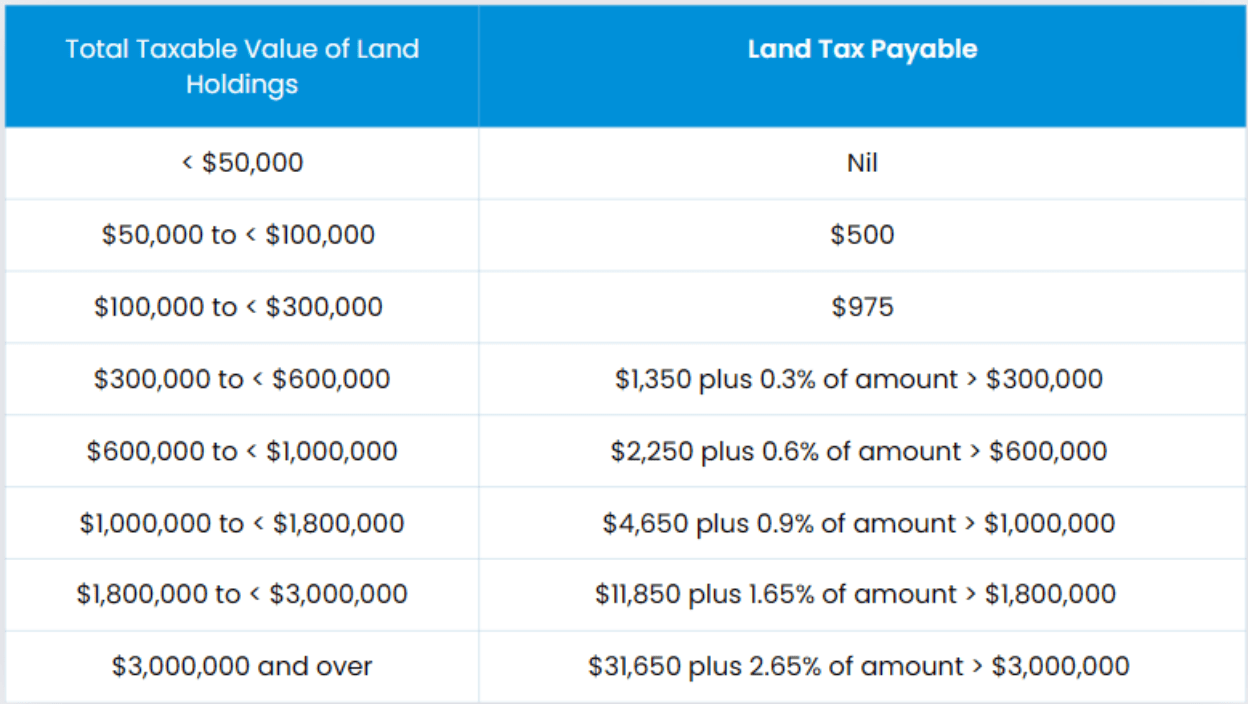

General Land Tax Rates (from 2024 land tax year)

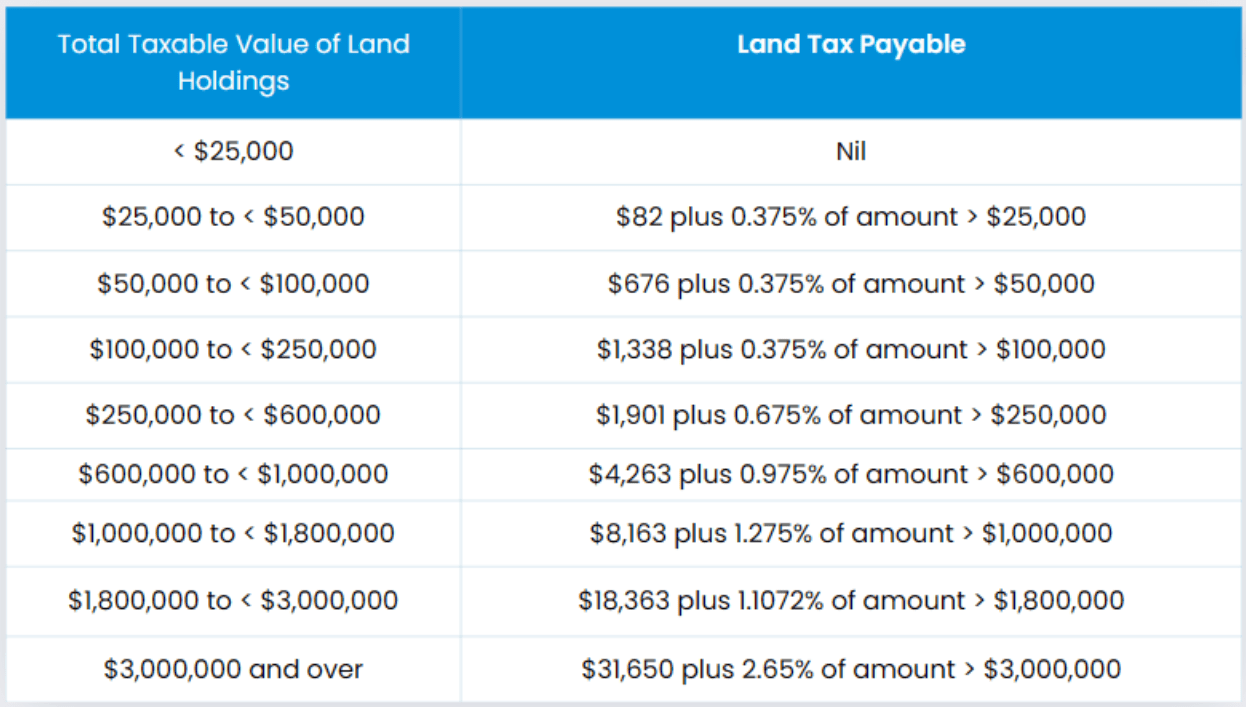

Land tax trust surcharge rates (from 2024 land tax year)

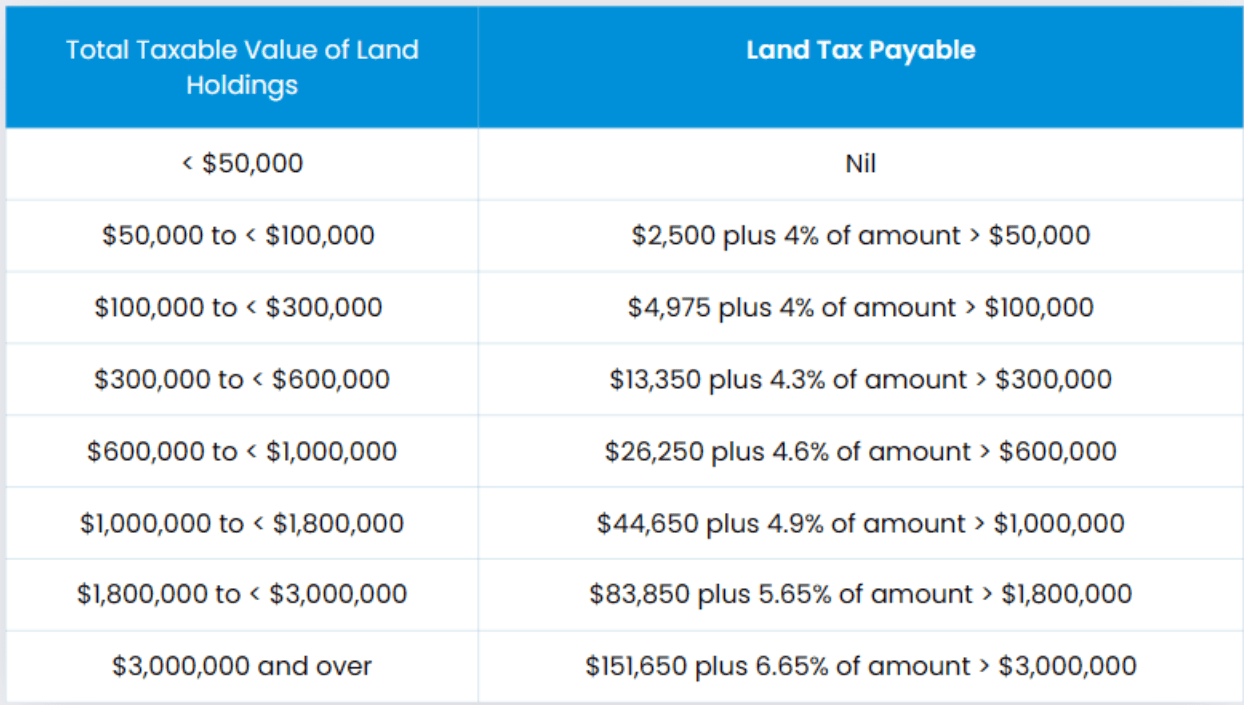

Land tax general rates with absentee owner surcharge (from 2024 land tax year)

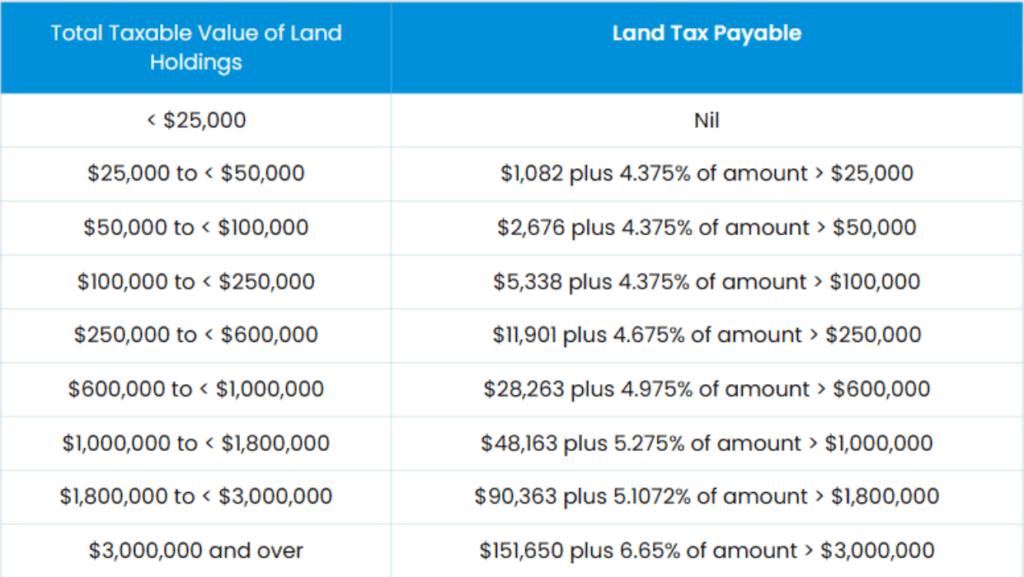

Trust surcharge rates for land tax with absentee owner surcharge (from 2024 land tax year)

Conclusion

The Victorian land tax system will see substantial changes in 2024, including new tax rates, the introduction of CIPT, and modifications to various property-related taxes. These changes are intended to establish a more equitable and efficient system for property taxation.

Property owners and developers must stay informed about these changes to manage their tax obligations effectively. Understanding the new rules and planning accordingly will be crucial to navigating the updated tax system.

These reforms represent a significant shift in Victoria’s property tax landscape. Property owners should seek advice from financial advisors or finance brokers in Sydney to understand the full implications and optimise their tax strategies.

For further guidance on how these changes may affect you, contact a mortgage broker or financial advisor today to ensure you’re prepared for the new tax landscape. Visit the official government tax website or consult with your local tax authority for more detailed information on these changes.