Ever feel like your mortgage is just dead weight holding you back from building wealth? For many Australians, homeownership is the biggest asset they have, but it’s also their biggest liability. A debt recycling strategy offers a smarter way to manage that balance. When done properly, it turns your home loan into a powerful tool to help you grow wealth, reduce tax, and potentially pay off your mortgage faster.

But here’s the catch: debt recycling only works if it’s structured correctly and tailored to your financial situation. In this guide, Unconditional Finance will walk you through how debt recycling works, how to set up your loan, and what the numbers look like in a real-world example. This is your starting point for debt recycling done right.

The Debt Recycling Process

Debt recycling works by gradually converting your non-deductible home loan, which doesn’t offer any tax advantages, into tax-deductible investment debt. In simple terms, it means you’re putting your mortgage to work, using equity to invest while still chipping away at the balance.

Imagine this: instead of just throwing all your spare income at the mortgage and waiting 25 years to be debt-free, you start recycling some of that effort into assets that could grow and generate returns. Over time, your home loan shrinks and your wealth grows.

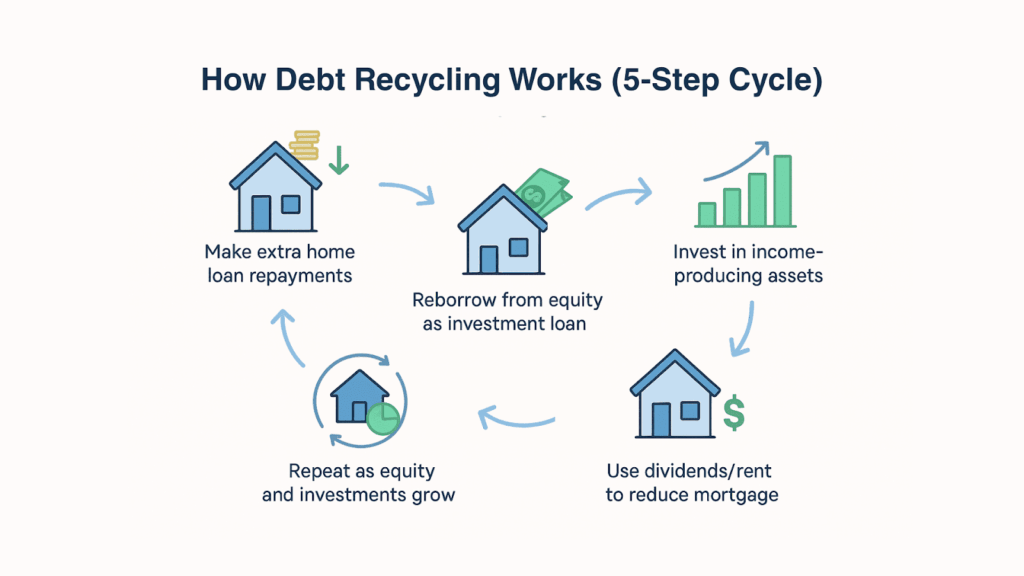

Here’s how the strategy typically plays out:

The 5-Step Cycle

- Make extra repayments on your home loan.

- Reborrow that repaid amount as a separate investment loan.

- Invest the borrowed funds into income-generating assets like ETFs, managed funds, or even investment property.

- Use any investment income (e.g. dividends or rent) to reduce your home loan even further.

- Repeat the process as your equity grows and your investments compound over time.

This cycle lets you grow your investment portfolio while continuing to pay down your home loan effectively. The longer you stick with it, the greater the potential snowball effect, reducing your mortgage faster and growing wealth at the same time.

Tip: Start small. Even $10,000 in reborrowed equity can begin the cycle. The strategy scales over time as equity and discipline build.

Not sure how this would look in your situation? Let’s map out a simple starting point based on your loan and equity.

How to Structure Your Loan for Debt Recycling

Debt recycling lives or dies by how well your loan is set up. If you’re using a basic home loan without redraw or split options, the strategy may not be feasible or worse, you could contaminate your tax deductions and lose the benefits entirely.

Split Loans: The Backbone of the Strategy

A split loan divides your home loan into two or more separate accounts:

- One for your owner-occupied mortgage (non-deductible)

- One for your investment borrowings (deductible)

This clear separation allows you to keep track of what’s being used for personal purposes and what’s being used for investing. The ATO requires this for any interest to be deductible.

Imagine this: you’ve got $600,000 remaining on your mortgage. You create a $100,000 loan split, and as you make extra repayments, you reborrow from that investment split to fund your ETF purchases. Now you’re keeping the strategy clean and ATO-compliant.

Important Setup Considerations

- Choose a lender that supports split loans with easy redraw or reborrow access.

- Label each split clearly in your internet banking (e.g. “ETF Loan”, “Shares”, “Property”).

- Avoid loan contamination by never mixing personal and investment expenses in the same split.

Not all banks allow flexible reborrowing. Some may require new loan applications every time you draw funds. Understanding how home equity loans work can help you assess whether your current loan setup supports debt recycling efficiently. A Sydney mortgage broker can help you identify lenders that offer the right features to support a debt recycling strategy over time.

What Debt Recycling Looks Like in Real Life (Cash Flow Example)

To understand the potential, let’s walk through a practical example. Say you’ve got:

- A $600,000 home loan

- An extra $1,000 per month available for repayments

- An interest rate of 6% (home and investment loan)

- A marginal tax rate of 37%

- You reborrow $50,000 to invest in a diversified ETF like VDHG, which we’ll assume returns 6.5% annually

Without debt recycling:

- Your $1,000 extra repayment just reduces the mortgage faster.

- You pay off the loan in ~22 years.

- You miss out on potential tax deductions and investment growth.

With a properly set-up debt recycling strategy:

- You reborrow and invest the $1,000 each month as you reduce your home loan.

- Investment income and tax savings help accelerate mortgage repayments.

- You still pay off the loan, but potentially in 17 to 18 years, while also building a portfolio worth $100,000 or more over time (depending on performance).

| Scenario | Mortgage Term | Tax Deduction Value | Investment Portfolio |

| No Debt Recycling | ~22 years | $0 | $0 |

| With Debt Recycling | ~17–18 years | ~$3,000/year | $100K+ (est.) |

These are illustrative figures only. Outcomes depend on returns, tax bracket, discipline, and borrowing structure.

When Debt Recycling Doesn’t Work

This isn’t a set-and-forget strategy, and it’s not for everyone. Even with the best loan structure, the strategy can backfire if it’s misused or if your financial circumstances aren’t stable.

You might want to rethink debt recycling if:

- You’re not good with budgets or struggle with credit card debt.

- You lack an emergency fund, and unexpected expenses could force you to sell your investments early.

- You’re likely to panic-sell during a market dip, locking in losses.

- You’re in a low tax bracket, so the interest deductibility provides minimal benefit.

If any of these red flags feel familiar, it doesn’t mean you’re out of options. It might just be time to pause and re-evaluate. Speak with an expert at Unconditional Finance to explore safer alternatives or build a pathway toward future readiness.

Get the Foundation Right First

Debt recycling has the potential to reduce your mortgage faster, build long-term wealth, and reduce tax, but only if it’s set up the right way from day one.

It starts with:

- Understanding the process

- Structuring your loan splits properly

- Staying consistent through market cycles

Thinking of trying it? Book a free debt recycling assessment, and let’s review your current loan setup and borrowing capacity.

Frequently Asked Questions (FAQs)

If you refinance or switch lenders, there’s a chance your existing loan splits or redraw structure may not carry over automatically. Some lenders treat reborrowing differently, and not all offer flexible split loan facilities that support ongoing debt recycling.

Before making any changes, it’s a good idea to check whether the new lender allows investment sub-loans, easy equity access, and redraws without triggering reassessment. Your mortgage broker can help you compare which home loans are more suitable for debt recycling in the Australian market.

You potentially can, although it depends on how your loan is set up. Offset accounts work by reducing the amount of interest charged on your home loan, which can support your overall repayment strategy. However, it doesn’t directly replace the role of a split loan in a debt recycling strategy.

Some borrowers use the offset to park surplus funds while maintaining redraw flexibility in their investment split. It’s important to separate funds clearly to maintain tax deductibility, and that often requires a more tailored setup. Speak to your broker or accountant to ensure your offset strategy aligns with your recycling goals.

It’s possible. Like any investment strategy, debt recycling comes with risks, especially during periods of market volatility. If the returns from your investments don’t keep pace with your loan interest costs, the strategy could reduce your overall cash flow.

That’s why it’s important to choose income-generating assets that suit your risk profile and investment timeframe. This approach tends to work better as a long-term strategy, where short-term fluctuations matter less than consistent performance over many years.

There’s no set rule, but lenders generally assess your ability to service both the home loan and the reborrowed investment portion. If you’re earning a stable income and have at least 20% equity in your property, you might be in a position to explore this strategy.

That said, your overall borrowing capacity, existing commitments, and risk tolerance all play a part. Even smaller equity amounts, like $10,000 to $20,000, can be enough to start, as long as the structure is right and you’re financially prepared.

Absolutely. One of the benefits of debt recycling is that it can be paused if your circumstances change, whether that’s due to job changes, family needs, or a market downturn. You can choose to stop reborrowing, keep your investments as-is, or redirect your focus entirely to paying off the home loan.

The key is ensuring your loan structure remains flexible, so you’re not locked into a strategy you can’t maintain. Always speak with your broker if your situation changes. There may be ways to adjust without undoing your progress.