Refinancing a mortgage can offer numerous benefits, such as lowering monthly payments, reducing interest rates, and shortening the loan term. These advantages can significantly enhance your financial stability and savings. However, for those with bad credit, the refinancing process presents unique challenges that can make these benefits harder to achieve. Understanding and overcoming these obstacles is necessary for making smart choices and boosting your success. This blog explores the challenges of refinancing with bad credit and provides practical strategies and tips to help you handle these challenges effectively.

At Unconditional Finance, we prioritise helping our clients reach their financial goals, no matter their credit score. Our team is dedicated to giving you personalised support and finding the best refinancing options for your needs.

With years of experience in the mortgage and finance industry, Unconditional Finance has the knowledge and resources to help you through the refinancing process. Our commitment to transparency, integrity, and client satisfaction, making us a trusted partner in achieving financial stability and success.

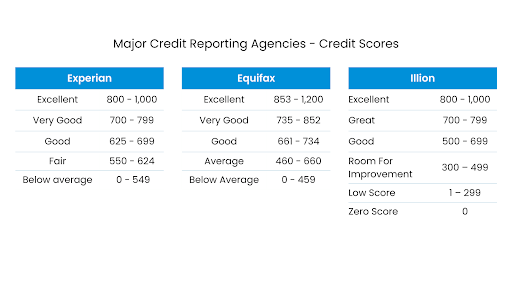

Understanding The Credit System in Australia

Before diving into the specifics of refinancing, it’s important to understand how the credit system works in Australia. Your credit score determines whether you can refinance and the terms you might get. Credit scores in Australia range from 0 to 1,200, assessed by major credit reporting agencies such as Experian, Equifax, and Illion. Here’s a breakdown of the categories:

If your score falls into the “Below Average” or “Average” categories, you’re considered to have bad or poor credit. Knowing your score can help you improve it or find better refinancing options.

The Challenges of Refinancing Mortgage With Bad Credit

Refinancing a mortgage with bad credit has unique obstacles that can make the process daunting. Understanding these challenges is the first step to finding good solutions. Here, we will explore the primary difficulties faced by homeowners with bad credit who are seeking to refinance.

1. Higher Interest Rates

For those who have bad credit, higher interest rates are almost certain. Lenders charge these rates to cover the risk of lending to borrowers with poor credit histories. While refinancing aims to reduce financial burdens, higher interest rates can negate these benefits. It’s essential to carefully calculate whether the potential savings from refinancing outweigh the costs of elevated interest rates.

2. Limited Lender Options

Having bad credit narrows your pool of potential lenders. Many lenders are hesitant to work with borrowers with a history of credit issues, limiting your options and making it harder to find favourable terms. This limitation can be frustrating, but persistence and thorough research can help you identify lenders specialising in working with individuals with less-than-perfect credit.

3. Strict Qualification Requirements

Lenders set stricter qualification criteria for borrowers with bad credit. These may include higher income requirements, larger cash reserves, and a lower debt-to-income ratio. Meeting these strict conditions can be challenging, but gathering all necessary documentation and presenting a strong case to potential lenders is crucial. Being well-prepared can improve your chances of securing a refinance.

4. Appraisal Issues

A home appraisal is a standard requirement during the refinancing process. If the value of your home has decreased since your initial purchase, it could complicate your ability to refinance, especially if you owe more on your mortgage than your home is worth now. This situation, known as being “underwater” on your mortgage, can be a significant barrier. However, some programs cater specifically to homeowners in this predicament, so exploring these options is worthwhile.

5. Private Mortgage Insurance (PMI)

If you have less than 20% home equity, you may be required to pay Private Mortgage Insurance (PMI), which adds to your monthly payments. This additional cost can make refinancing less attractive, especially if you already have higher interest rates. Calculating the overall impact of PMI on your financial situation is important before deciding to refinance.

6. Closing Costs

Refinancing isn’t free; it involves various fees and closing costs that can be substantial. For borrowers with bad credit, coming up with these upfront costs can be particularly challenging. It’s essential to factor these expenses into your refinancing decision and consider whether you can cover them without compromising your financial stability.

7. Negative Impact on Credit Score

Refinancing involves multiple credit inquiries, which can further lower your credit score. Any late payments or defaults on your existing mortgage can negatively impact your credit, making it even harder to secure favourable terms. To avoid this risk, pay your mortgage on time and improve your credit score before refinance.

8. Longer Approval Process

Borrowers with bad credit often need a longer approval process as lenders require more documentation and thorough scrutiny of their financial situation. This extended timeline can add stress and uncertainty to an already challenging process. Being organised and responsive to lender requests can help expedite the approval process.

9. Higher Risk of Rejection

Due to poor credit history, there’s a higher likelihood of being denied for a refinance. Rejection can be discouraging and might limit your refinancing opportunities. However, understanding the reasons for rejection and working to address them can improve your chances in future applications.

10. Potential for Predatory Lending

Borrowers with bad credit may be targeted by predatory lenders offering unfavourable terms and high fees. It’s crucial to be cautious and thoroughly review the terms of any refinancing offer. Seeking advice from reputable financial advisors can help avoid predatory lending traps.

Strategies for Success in Refinancing with Bad Credit

Refinancing a mortgage with bad credit may seem challenging, but with the right strategies, it’s possible to secure better terms and improve your financial situation. Here are some strategies to increase your chances of success when refinancing with bad credit.

1. Shop Around for Lenders

One of the most important steps in refinancing with bad credit is to shop around for lenders. Different lenders have different rules and offers, so it’s important to research and compare several options. This helps you find the best option for your needs.

2. Consider FHA or VA Loan

If you qualify, FHA (Federal Housing Administration) and VA (Veterans Affairs) loans can be excellent options. These loans usually have easier credit requirements and might offer better terms for those with bad credit. FHA and VA loans can make refinancing more accessible and affordable.

3. Opt for a Co-Signer

Another effective strategy is to opt for a co-signer with good credit. A co-signer can greatly improve your chances of getting approved and help you get better terms. This shows lenders there’s extra security, making them more likely to offer favourable conditions.

4. Look for Lenders Specialising in Bad Credit

Some lenders focus on helping borrowers with bad credit. These lenders might offer more flexible terms and conditions. It’s worth finding lenders specialising in bad credit to get refinancing options that fit your needs.

5. Negotiate Terms

Feel confident to ask for better terms when refinancing. Lenders might lower interest rates or fees to win your business. Effective negotiation can improve terms, making the refinancing process more beneficial.

6. Use a Mortgage Broker

A mortgage broker can be a great help in the refinancing process. Brokers can guide you through the details and find lenders who will work with your credit. They know many lenders and can make the process quicker and easier.

Tips for Improving Chances of Refinancing

Enhancing your chances of refinancing with bad credit involves taking proactive steps to improve your financial profile. Here are some tips to help you prepare and increase your likelihood of success.

1. Improve Your Credit Score

Improving your credit score is one of the most impactful steps. Here are specific actions to help you achieve this:

- Fix Errors on Your Credit Report: Obtain your credit report from major credit reporting agencies (Experian, Equifax, and Illion). Carefully review the report for errors or discrepancies and dispute them.

- Obtain your credit report.

- Identify errors (e.g., incorrect accounts, wrong balances).

- File disputes with the credit agencies, providing necessary documentation.

- Follow up until disputes are resolved.

- Set Up Automatic Payments: Ensure you never miss a payment by scheduling automatic bill payments.

- Log in to your bank account.

- Navigate to the bill pay or auto-pay section.

- Set up automatic payments for recurring bills.

- Pay Down Outstanding Debt: Focus on paying high interest rates first, like credit card balances.

- List all debts with their interest rates.

- Prioritise paying off high-interest debts.

- Pay extra on your loan to pay off the balance quicker.

- Avoid New Credit Inquiries: Limit applications for new credit to prevent additional hard inquiries on your report.

- Avoid getting new credit cards or loans.

- Consult with a financial advisor before making any new applications.

2. Increase Home Equity

Increasing your home equity can make refinancing more attractive. Here’s how you can do it:

- Pay Down Your Mortgage Principal: Make extra payments towards your mortgage principal whenever possible.

- Ask your lender to make sure there are no penalties for paying off your loan early.

- Allocate extra funds to your principal payment each month.

- Consider Home Improvements: Invest in home improvements that increase your property’s value.

- Identify cost-effective improvements (e.g., kitchen remodel, landscaping).

- Get quotes from contractors and choose the best option.

- Implement the improvements and keep records of the enhancements.

3. Reduce Your Debt-to-Income Ratio

Lenders look closely at your debt-to-income ratio. Here’s how you can improve it:

- Pay Off Existing Debts: Focus on reducing your current debt load.

- List all debts and their monthly payments.

- Create a budget to allocate extra funds towards debt repayment.

- Use windfalls (e.g., tax refunds, bonuses) to pay down debt.

- Don’t Take On New Debt: Resist the temptation to take on new debt before and during refinancing.

- Avoid large purchases that require financing.

- Delay opening new credit accounts until after the refinancing process is complete.

4. Prepare a Strong Financial Profile

Gather and organise all necessary financial documents to present a strong case to lenders. Here’s how:

- Collect Financial Documents: Ensure you have all the necessary documents, like tax returns, pay stubs, and bank statements.

- Collect your tax returns from the past two years.

- Collect recent pay stubs (last two months).

- Compile bank statements for the past three to six months.

- Organise these documents in a folder or digital file for easy access.

- Show Stable and Sufficient Income: Provide proof of steady income to reassure lenders of your ability to repay the loan.

- Highlight your income stability in your application.

- Include additional income sources (e.g., rental income, side jobs).

5. Save for Closing Costs

Refinancing involves fees and closing costs, typically 2% to 5% of the loan amount. Here’s how to prepare:

- Budget for Closing Costs: Estimate the total closing costs and save accordingly.

- Request an estimate of closing costs from potential lenders.

- Create a savings plan to set aside the required amount.

- Keep these funds in a separate account to ensure they are readily available.

6. Consider a Bigger Down Payment

Making a bigger down payment can increase your chances of getting approved and better terms. Here’s how:

- Allocate Extra Funds for Down Payment: Save additional money to increase your payment.

- Assess your savings and determine how much more you can allocate.

- Make a plan to save the additional amount before refinancing.

- Present this larger down payment to the lender to improve your terms.

7. Seek Professional Advice

Consulting a credit counsellor or financial advisor can give you personalised advice. Here’s how:

- Find a Qualified Advisor: Find a reputable financial advisor or credit counsellor.

- Research and select a financial advisor or credit counsellor.

- Schedule a consultation to discuss your refinancing goals and credit improvement strategies.

- Follow their advice and create a plan tailored to your situation.

8. Stay Employed and Stable

Maintaining steady employment and income stability is crucial. Here’s how:

- Avoid Job Changes: Try to stay in your current job during the refinancing process.

- Communicate with your employer about your plans to refinance.

- Only make significant job changes after the refinancing is complete.

- Highlight your employment stability in your application.

Conclusion

Refinancing a mortgage with bad credit takes careful planning and smart strategies. By understanding the challenges, such as higher interest rates, limited lender options, and stricter qualification requirements, you can better prepare yourself for the process. Remember to shop around for lenders, consider special loan programs, improve your credit score, and seek professional advice to enhance your refinancing prospects. Acting now can lead to better financial results later. If you’re considering refinancing, contact a financial advisor or mortgage brokers in Sydney to discuss your situation and develop a tailored plan for success.

Ready to Refinance Your Mortgage with Bad Credit?

Don’t let bad credit hold you back from refinancing your mortgage. With the right strategies and support, you can overcome the challenges and secure better terms. Contact us now to discuss your refinancing goals and find the best solutions for your financial future. Let’s work together to turn your refinancing challenges into opportunities for success!

FAQs

Can you refinance with a bad credit score? Yes, you can refinance even with a bad credit score. However, you may face higher interest rates and more stringent qualification requirements. Shopping around for lenders specialising in bad credit refinancing can help you find better terms.

Is it possible to refinance my mortgage if I have bad credit in Australia? Yes, refinancing with bad credit in Australia is possible. You should explore options like FHA or VA loans or look for lenders specialising in working with individuals with poor credit.

Will I automatically get higher interest rates because of my bad credit? Lenders usually charge higher interest rates to protect themselves when lending to people with bad credit. But you can get better deals by improving your credit score and negotiating,

How can I improve my credit score before refinancing? Improve your credit score by paying off debts, making timely payments, not applying for new credit, and correcting errors on your credit report. Good credit habits over time will also help.

Does every credit application harm my score? Yes, your score can drop slightly each time you apply for credit. However, if you shop for rates within a short period (typically 14-45 days), multiple inquiries are often treated as a single inquiry, minimising the impact on your score.

What is a credit utilisation ratio, and why is it important? The credit utilisation ratio is how much of your available credit you use. It’s important for your credit score. Keeping this ratio below 30% can improve your credit score.

Should I consult with a financial expert before refinancing? Yes, consulting with a financial expert or credit counsellor can provide personalised advice and strategies to improve your credit and increase your chances of successful refinancing.

Are there specific mortgage programs tailored for individuals with bad credit? Yes, loans like FHA and VA often have easier credit requirements and are good for people with bad credit. Some lenders also specialise in helping those with poor credit.

What are the common challenges individuals with bad credit face when attempting to refinance a mortgage? Common challenges include higher interest rates, limited lender options, stricter qualification requirements, potential appraisal issues, the need for PMI, significant closing costs, a negative impact on credit score, longer approval processes, higher risk of rejection, and the threat of predatory lending.

Should I wait and improve my credit score before attempting to refinance, or should I start the process now? It depends on your financial situation and goals. You might get better terms if you wait and improve your credit score. But if you need financial help immediately, you can start the process now while working on your credit. Simultaneously, working on improving your credit can be a viable approach.

Can I refinance with bad credit if I’ve previously missed mortgage payments? Yes, you can refinance, but missed mortgage payments make it harder. Lenders will check your overall credit history. Showing recent improvements in your credit and financial stability can help.