For many Australians, owning a home is a cherished dream, yet rising property prices have made this dream increasingly elusive. Enter the First Home Guarantee Scheme (FHGS), a government initiative designed to turn this dream into reality. The FHGS helps first-time homebuyers secure a home loan with a smaller deposit by guaranteeing a portion of their loan, thus eliminating the need for Lenders Mortgage Insurance (LMI).

At Unconditional Finance, we prioritise empowering our clients with the knowledge and tools they need to navigate the complex world of home buying. Our skilled brokers are here to give you personalised help and advice, so you can make smart choices about your finances.

We understand that purchasing a home is one of the most significant investments you will ever make. That’s why we are committed to helping you find the right mortgage options that fit your specific needs. Whether you are a first-time buyer or looking to upgrade, Unconditional Finance is here to assist you every step of the way.

With the recent expansion to 50,000 new places for the 2024-2025 fiscal year, the scheme has opened up new opportunities for Australians. However, significant challenges remain. Finance brokers like Chris Raymond and Sandy Paravizzini have voiced concerns about the scheme’s limitations, particularly the strict income and property price caps. This blog delves into these challenges, the insights provided by industry experts, and potential solutions to make the scheme more effective.

The First Home Guarantee Scheme: An Overview

The FHGS allows eligible buyers to secure a home loan with a deposit as low as 5% without needing Lenders Mortgage Insurance (LMI). The government guarantees up to 15% of the property value, making it easier for buyers to enter the housing market.

Eligibility Criteria

- Citizenship and Residency: To apply, you must be an Australian citizens or have permanent residency.

- Age: You must be 18 years or older to apply.

- Income: For individuals, the maximum taxable income is $125,000, and for joint applicants, it is $200,000, as shown on the Notice of Assessment.

- Ownership Status: Applicants must be first-time homebuyers or individuals who haven’t owned a property in the past ten years.

- Occupancy: The purchased property must be intended for owner-occupation.

Eligibility Considerations

- First-time Homebuyer Definition: A first-time homebuyer has never owned a property, whether it’s an investment or a primary residence. This includes any co-ownership situations. Definitions can vary slightly by region, so it’s essential to check local guidelines.

- Proving Eligibility: Applicants must provide documentation, such as tax returns, proof of residency, and other financial statements. This process ensures that only those who genuinely need assistance benefit from the scheme.

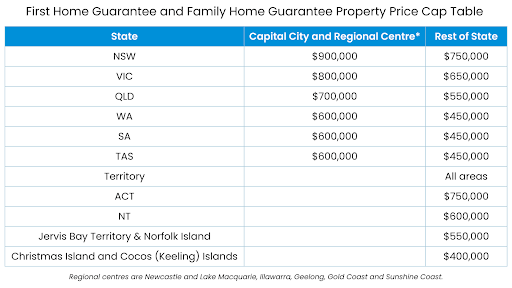

Property Price Caps

Property price caps vary by state and region to ensure the scheme targets those who need it most. However, these caps also create significant limitations, especially in high-demand property markets.

Source: Housing Australia

Current Challenges Highlighted by Brokers

Chris Raymond, a lead broker, recently highlighted the challenges faced by brokers and their clients under the current FHGS framework. He noted that while the scheme was highly popular at its launch, its appeal has waned in NSW due to escalating house prices.

Raymond explained that few clients qualify due to income and loan requirements. In the 2024 fiscal year, only about 2% of the brokerage’s settlements fell under the FHGS requirements. Most eligible clients were singles or couples without dependents, underscoring the restrictive nature of the scheme’s criteria.

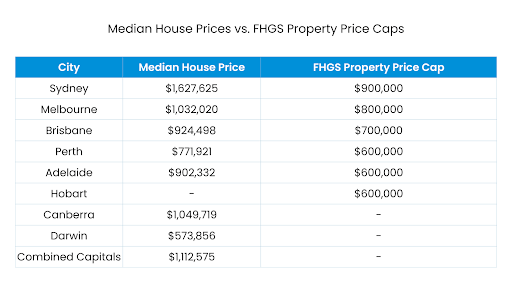

Statistical Insights

The data shared by Raymond underscores the scheme’s limitations. With only 2% of settlements qualifying under the FHGS, it’s evident that the income and property price caps are not in sync with current market conditions. For instance, the median house price in Sydney is close to $1.6 million. Yet, the maximum income for a single person to qualify for the scheme in Sydney is $125,000, or $200,000 for a couple. This discrepancy significantly reduces the pool of eligible first-time buyers.

Source: Housing Australia, Domain

Broker Recommendations for Improvement

Increase Income and Property Price Caps

Raising income caps to match today’s higher earning thresholds is crucial. This change would allow more individuals and couples to qualify for the scheme, particularly in high-cost areas where even moderate-income earners struggle to save for a deposit. Updating the property price caps to align with the current median prices in major cities is also essential. This adjustment would make it feasible for buyers to find properties within the scheme’s limits, thereby increasing the scheme’s accessibility and effectiveness.

Regional Adjustments and Regular Reviews

Consider varying the caps not just by state but by specific regions within states to account for local market differences. This could make the scheme more equitable and accessible across diverse property markets, ensuring that it supports buyers in both high-cost urban areas and more affordable regional markets. Implementing a system for regular reviews and updates of the scheme’s criteria to ensure they remain relevant to the changing market conditions is crucial. This proactive approach could prevent the scheme from becoming outdated and ineffective, ensuring that it continues to serve its intended purpose over the long term.

Potential Solutions and Broader Impact

A Tiered Cap System

One innovative solution could be a tiered cap system that sets different price caps for different regions within each state. This approach would acknowledge the significant variations in property prices across regions, ensuring that the scheme remains relevant and accessible to buyers in both high-cost and lower-cost areas.

Enhanced Data Analytics and Collaboration

Utilising enhanced data analytics to regularly assess and adjust the income and property price caps could ensure that the FHGS remains in sync with market conditions. Using real-time data on housing prices and economic trends, policymakers can create better plans to help first-time homebuyers. Collaboration between the government and financial institutions could also enhance the scheme’s effectiveness. For instance, creating tailored loan products that complement the FHGS, with features such as reduced interest rates or longer repayment terms, could help bridge the affordability gap for first-time buyers.

Conclusion

The First Home Guarantee Scheme remains a vital tool in helping Australians achieve homeownership. However, as highlighted by industry experts like Chris Raymond, it is clear that the scheme’s current criteria need revision to better align with today’s property market realities. Increasing the income and property price caps, along with implementing more region-specific adjustments and regular updates, could significantly enhance the scheme’s effectiveness.

By addressing these challenges and making necessary adjustments, policymakers can ensure that the FHGS continues to support first-time homebuyers across Australia, helping more individuals and families secure their dream homes. The scheme’s success depends on its ability to change and grow with the housing market, making sure it stays a strong support system for those who need it.

Want to start your journey to owning a home? Contact our expert brokers today to learn how the First Home Guarantee Scheme can work for you!

FAQS

1. What is the First Home Guarantee Scheme (FHGS)?

The First Home Guarantee Scheme (FHGS) is a government initiative designed to help first-time homebuyers secure a home loan with a smaller deposit. The government guarantees a portion of the loan, eliminating the need for Lenders Mortgage Insurance (LMI).

2. How does the FHGS help first-time homebuyers?

The FHGS allows eligible buyers to secure a home loan with a deposit as low as 5%, with the government guaranteeing up to 15% of the property value. This reduces the need for LMI, making it simpler and cheaper for first-time buyers to enter the housing market.

3. Who is eligible for the FHGS?

Eligibility criteria for the FHGS include:

- Australian citizenship or permanent residency.

- Minimum age of 18 years.

- Maximum taxable income of $125,000 for individuals and $200,000 for joint applicants.

- Must be a first-time homebuyer or not have owned a property in the past ten years.

- The purchased property must be intended for owner-occupation.

4. What documentation do I need to prove eligibility?

To prove their eligibility for the scheme, applicants must provide documentation such as tax returns, proof of residency, and other financial statements.

5. What are the property price caps under the FHGS?

Property price caps vary by state and region to target those who need the scheme most. These caps are designed to ensure the scheme benefits eligible buyers in high-demand property markets but can limit accessibility in certain areas.

6. What challenges does the FHGS face?

Key challenges include:

- Strict income and property price caps that may not align with current market conditions.

- Limited eligibility for buyers in high-cost areas like Sydney due to high property prices and income restrictions.

7. How can the FHGS be improved?

Brokers recommend increasing the income and property price caps to reflect higher earning thresholds and median property prices. They also suggest regular reviews and regional adjustments to ensure the scheme remains relevant and accessible.

8. What is a tiered cap system?

A tiered cap system sets different property price caps for different regions within each state. This approach acknowledges variations in property prices and ensures the scheme remains accessible to buyers in both high-cost and lower-cost areas.

9. How can data analytics improve the FHGS?

Enhanced data analytics can help regularly assess and adjust income and property price caps based on real-time housing prices and economic trends. This ensures the scheme stays in sync with market conditions.

10. Can the FHGS help with loan product customisation?

Yes, a collaboration between the government and financial institutions can create tailored loan products that complement the FHGS. These products might offer reduced interest rates or longer repayment terms, making homeownership more affordable for first-time buyers.

11. How often are the FHGS criteria reviewed and updated?

Implementing a system for regular reviews and updates is crucial to ensure the FHGS criteria remain relevant to changing market conditions. This proactive approach can prevent the scheme from becoming outdated and ineffective.

12. How can I apply for the FHGS?

To apply for the FHGS, contact an expert broker who can guide you through the eligibility criteria, required documentation, and application process.