Have you ever pondered the possibility of whether refinancing your home is the right strategic move for your financial future? It’s a contemplation that occupies the minds of many homeowners, given its potential to profoundly influence your fiscal destiny. One frequently underestimated facet is comprehending the eligibility criteria linked to home refinancing. In this piece, we’ll walk you through the imperative nature of understanding these criteria before plunging into the realm of refinancing. So what are the criteria for refinancing a home? Let’s get started!

Importance of Understanding Eligibility Criteria Before Home Refinancing

Before you set forth on the path to refinance your home, it’s imperative to fully comprehend the eligibility criteria at play. This comprehension not only streamlines the entire process but also guarantees that your decision is backed by a thorough understanding. Eligibility criteria serve as a set of directives that lenders utilise to gauge whether you meet the requirements for refinancing a home. By acquainting yourself with these criteria, you equip yourself to confidently navigate the refinancing landscape, making well-informed decisions that align with your financial goals. Do these before jumping in:

- Property Appraisal: Conduct a comprehensive assessment of your property’s value to bolster your chances.

- Income Documentation: Ensure you have robust documentation, including pay stubs and tax returns, to demonstrate your income stability.

- Credit Score Management: Proactively manage your credit, addressing any discrepancies and improving your score before embarking on refinancing.

- Debt Reduction: Strategically pay off existing debts to enhance your debt-to-income ratio, showcasing financial responsibility to lenders.

Looking ahead, implementing these strategies not only simplifies your current refinancing process but lays a foundation for future financial endeavors. By cultivating a habit of proactive financial management, you position yourself to navigate potential refinancing opportunities with ease, ensuring a smoother and more efficient process for your financial future.

Current Trends in the Australian Refinancing Market

Australia’s refinancing landscape is an ever-changing tapestry woven with economic nuances and trends. To optimise your refinancing journey, immerse yourself in the pulsating rhythm of the Australian market. The dynamics are multifaceted, driven by economic forces that demand your attention. Let’s delve into the key trends shaping the Australian refinancing sphere:

- Interest Rate Fluctuations: Track the ebb and flow of interest rates, as they play a pivotal role in determining the cost-effectiveness of refinancing.

- Economic Conditions: Understand the broader economic landscape, considering factors such as employment rates and GDP growth, to gauge the market’s stability.

- Government Policy Impact: Stay attuned to government policies, which can sway the market’s direction, influencing the regulatory environment for refinancing.

- Lender Offerings: Stay vigilant about lenders’ evolving products and offerings aligning with market trends and diverse borrower needs. Understanding the requirements for refinancing a house is crucial, ensuring you can make informed decisions in response to changing market dynamics.

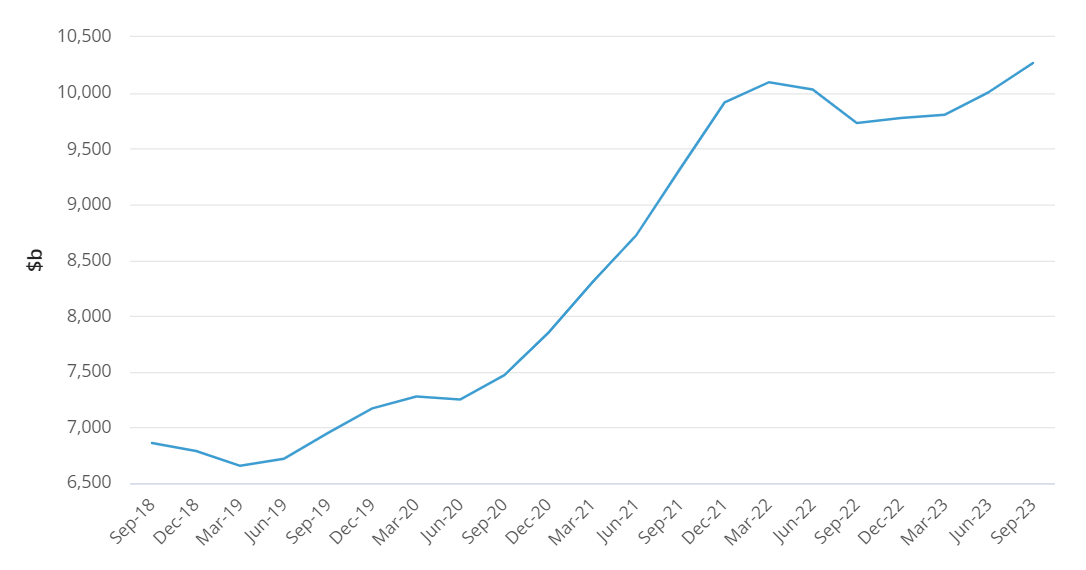

The latest data on Australia’s housing market collected by ABS reveals positive trends. In the September quarter of 2023, residential dwelling values increased by $261.0 billion to reach $10,267.4 billion. The number of dwellings also rose by 52,300, totaling 11,094,500, with a mean price increase of $19,200 to $925,400. All states and territories experienced growth in the total value of residential dwellings, reflecting a robust housing market. Of this total, households owned $9,863.4 billion, showcasing widespread growth across the country.

Amidst this favorable landscape, participating wisely in the refinancing arena goes beyond the present to anticipate the future. The Australian refinancing market is dynamic, and your success hinges on surfing its waves. Amidst this favorable landscape, participating wisely in the refinancing arena goes beyond the present to anticipate the future. The Australian refinancing market is dynamic, and your success hinges on surfing its waves.

Key Qualification Criteria for Refinancing

Now, let’s delve into the key criteria for refinancing home that lenders typically consider when evaluating a refinancing application. First and foremost is assessing the equity in your property. Lenders often prefer homeowners with a significant amount of equity, as it provides them with security. Additionally, your income stability and employment status play a pivotal role. Demonstrating a steady income stream and stable employment enhances your eligibility for refinancing.

Evaluating the property’s equity

Delving into the realm of property equity, we find it to be an indispensable facet in the intricacies of the refinancing process. Lenders actively seek a noteworthy equity quotient, considering it a protective measure. To gauge your property’s equity, a judicious approach involves conducting a home appraisal or seeking counsel from a real estate professional. Nurturing an understanding of your property’s equity not only becomes an insightful endeavor but also augments your prospects of securing an advantageous criteria for refinancing home arrangement.

Assessing Income Stability and Employment Status

Turning our attention to the fundamental bedrocks of your financial profile – income stability and employment status – we encounter elements pivotal to lenders. Their objective is to verify the presence of a dependable income source capable of servicing the refinanced loan. Prior to initiating the refinancing application, it becomes imperative to conduct a comprehensive self-assessment of your income stability. This necessitates furnishing supporting documentation, encompassing pay stubs, tax returns, and employment verification.

Examining Property Value

Moving beyond equity, lenders broaden their examination to assess the overall value of your property. The current market value of your home significantly shapes the loan-to-value ratio, a crucial element in refinancing. Keep a watchful eye on local property values, preparing for a potential appraisal. Understanding how lenders evaluate property value strategically positions you in the dynamic refinancing landscape.

Identifying Necessary Paperwork

Transitioning to a pivotal step, gathering essential paperwork stands out as a crucial milestone in your refinancing journey. As one of the requirements for refinancing a home lenders require a careful compilation of documents to validate your financial status and eligibility. Anticipate requests for proof of income, employment history, property details, and other relevant documents. Prudent preparation with the necessary paperwork in advance acts as a catalyst, simplifying the refinancing application and approval process. Ensuring your documents are organised and readily accessible not only expedites the process but also reflects positively on your diligence as a borrower.

Tips for Success in the Process

As you navigate the refinancing journey, consider integrating these recommendations for a prosperous outcome. Actively managing your credit is crucial, as an elevated credit score can pave the way for more favorable terms. Furthermore, settling outstanding debts prior to refinancing applications can enhance your debt-to-income ratio, boosting your eligibility. Finally, don’t hesitate to solicit advice from financial experts or mortgage professionals to guarantee well-informed decision-making.

Proactively Managing Credit

Your credit score assumes a pivotal role throughout the refinancing adventure. Take preemptive measures to oversee and enhance your creditworthiness before applying. Timely bill payments, reduction of outstanding debts, and rectifying any discrepancies on your credit report can substantially influence your credit score, heightening the likelihood of securing a favorable refinancing arrangement.

Paying Off Other Debts Before Applying

Trimming your overall debt load stands as a judicious strategy before venturing into the refinancing landscape. Lenders scrutinise your debt-to-income ratio, and settling existing debts can positively reshape your financial profile. This strategic move communicates to lenders that you embody responsible borrowing habits, elevating your chances of receiving approval for requirements for refinancing a mortgage.

Seeking Advice from Experts

When uncertainty clouds your path, seek counsel from financial experts or mortgage professionals. Navigating the complexities of the refinancing process can be daunting, and expert advice offers invaluable perspectives. Engage with professionals specialising in mortgage refinancing to ensure your decisions align seamlessly with your unique financial goals and circumstances.

Final Thoughts

Refinancing your home is a transformative financial journey. Key to informed decisions is understanding eligibility criteria, including property equity and income stability. In the dynamic Australian refinancing market, stay proactive, anticipate shifts, and capitalise on emerging opportunities. Focus on refining property equity, aligning income stability with lender expectations, and streamlining the process through meticulous paperwork. Manage credit actively, settle debts responsibly, and seek expert guidance to showcase financial responsibility. This guide empowers your current refinancing and establishes a resilient foundation for your financial future.

FAQ

1. What are common requirements for refinancing?

Understanding the prerequisites for refinancing is crucial. Lenders typically look for a credit score of 620 or higher, a debt-to-income ratio below 43%, and a loan-to-value ratio below 80%. Additionally, a stable income, employment history, and a favorable property appraisal are key factors.

2. What conditions should be met for refinancing?

Meeting specific conditions is essential in the refinancing process. Ensure you have a decent credit score, a manageable debt-to-income ratio, and a loan-to-value ratio that reflects sufficient equity. A stable income, steady employment, and a positive property appraisal contribute to meeting the necessary conditions.

3. What is not an advisable reason to refinance?

While refinancing can be advantageous, it’s not advisable to do so solely for frivolous reasons. Using refinancing as a means to fund a lavish lifestyle or unnecessary expenses is imprudent. It’s essential to refinance with a clear financial goal, such as securing a lower interest rate or consolidating high-interest debt.

4. What is the optimal scenario for refinancing?

The best scenario for refinancing is when interest rates are significantly lower than your current mortgage rate. This can result in substantial savings over the life of the loan. Additionally, a good credit score, improved financial health, and a long-term commitment to the property contribute to an optimal refinancing situation.